Idiotic shoppers

Warning: For Full Access Please Log In or Create an Account (Free)

@FrugalCat wrote:

I am the idiot. Yes, I take the MF grocery shops for $0. Since COVID-the fee has disappeared. Rarely there is a $5 fee put on the shop- usually for the last minute assignments that someone else flaked on. I take these shops at no fee as I need groceries. During the pandemic, I was spending a ton of money at supermarkets (I stopped dining out or even getting takeout). The shops are super-easy, as I am used to asking the stupid questions and filling out the report- I was doing the grocery shops for about 5 years pre-pandemic. Call me an idiot if you must, but these grocery shops feed me and my family. Sure, it would be nice to have a fee or bonuses. Now if you'll excuse me, I have a shop today and every day for the rest of the week.

If you wait a few days, they move the grocery shops up on the list and add $5 or $8 for the shop payment. All you have to do is wait a few days, stop self-assigning them until after they add the shop payment. That's ALL it takes is to wait a couple days. Stop selling yourself short and stop cheating the rest of us out of paying work. I don't generally do them at $8 either, I wait for them to call me to offer them at $15 or higher both pre and "post" covid.

How is the shopper who takes shops for no or low fee cheating you or anyone else out of paying work? You claim that you wait for higher fees! You have work! You wait until you like the sum you will be paid for it! You also might have a larger tax bill later, or at least have to finagle a smaller one. Perhaps it is time for a new definition of idiot: a person who is so stupid that they acquire quantities of free stuff in exchange for being observant and multi-tasking while performing a typical life chore and reporting on observations, while incurring little or no tax liability and, depending upon circumstances, possibly gaining a tax deduction or other advantage at tax time as this pertains to travel method and the location of work. Yes. That is an idiot.

@Morledzep wrote:

@FrugalCat wrote:

I am the idiot. Yes, I take the MF grocery shops for $0. Since COVID-the fee has disappeared. Rarely there is a $5 fee put on the shop- usually for the last minute assignments that someone else flaked on. I take these shops at no fee as I need groceries. During the pandemic, I was spending a ton of money at supermarkets (I stopped dining out or even getting takeout). The shops are super-easy, as I am used to asking the stupid questions and filling out the report- I was doing the grocery shops for about 5 years pre-pandemic. Call me an idiot if you must, but these grocery shops feed me and my family. Sure, it would be nice to have a fee or bonuses. Now if you'll excuse me, I have a shop today and every day for the rest of the week.

If you wait a few days, they move the grocery shops up on the list and add $5 or $8 for the shop payment. All you have to do is wait a few days, stop self-assigning them until after they add the shop payment. That's ALL it takes is to wait a couple days. Stop selling yourself short and stop cheating the rest of us out of paying work. I don't generally do them at $8 either, I wait for them to call me to offer them at $15 or higher both pre and "post" covid.

Pronoun, schmonoun. I am a female human.

Well, I don't know about you guys but I feel alot more pressure now to take shops at base or small bonuses because if I don't, someone else will. There are still many that that I don't take because the pay is way too low but someone near me takes them. If I wait for a bonus on a job I want, as mentioned above, I probably would not get the job at all.

A lot of it speaks to economic desperation and powerlessness too.

Workers in America are relatively poor (compared to 40-50 years ago, before corporations took over Congress and crushed the working and middle-class and unions). Brookings Institute (non-partisan) found that:

[www.brookings.edu] (Nov. 2019)

There aren't enough "good jobs" to go around for non-college degree workers:

It feels like everyone I know doing some form of gig work complains from time-to-time of making crap wages. I tend to think the "desperation" you're seeing in people is more tied to structural economic issues vs. just plain stupidity. It's not that easy for some to just "find another good paying job," yet, in the meantime, they have bills to pay and/or savings they want to build.

For sure, I think some MSCs offer offensive/predatory compensation too. I don't think they can look at shoppers with a straight face and think $1.00 shops are totally fair. They are also just operating on supply and demand in the absence of a min. wage for the industry. And shoppers are desperate in America.

Workers in America are relatively poor (compared to 40-50 years ago, before corporations took over Congress and crushed the working and middle-class and unions). Brookings Institute (non-partisan) found that:

[www.brookings.edu] (Nov. 2019)

[www.brookings.edu] (also Nov. 2019)@ wrote:

An estimated 53 million people—44 percent of all U.S. workers ages 18–64—are low-wage workers. That’s more than twice the number of people in the 10 most populous U.S. cities combined. Their median hourly wage is $10.22, and their median annual earnings are $17,950.

There aren't enough "good jobs" to go around for non-college degree workers:

Gig work like ms-ing is likely plugging income holes for a lot of Americans. Even my sister and cousin, who both teach elementary, have part-time and gig work jobs they do at night/weekends. They need/like the flexibility of it, since they can't really commit to regular hours of a second stable job (at least not until the summer), but they sometimes make less than min. wage on these jobs (sometimes in the $6.50 - $7/hour range from what we calculated).@ wrote:

Recent analysis by our Metropolitan Policy Program colleagues as well as researchers at the Federal Reserve suggest that there simply are not enough jobs paying decent wages for people without college degrees (who make up the majority of the labor force) to escape low-wage work.

Our colleagues Chad Shearer and Isha Shah identified good jobs for workers without bachelor’s degrees by defining “good jobs” as those paying median earnings or more for a given metropolitan area and providing health insurance. They found that such jobs are relatively scarce, held by only 20% of workers without bachelor’s degrees in large metro areas. Another 13% are in “promising” jobs, in which incumbent workers are likely to progress to a good job within 10 years.

An analysis by Kyle Fee, Keith Wardrip, and Lisa Nelson came to similar findings. They defined good jobs for workers without a bachelor’s degree as those paying at least the national median wage adjusted for local cost of living. The analysis found that for every good job there are 3.4 working-age adults with less than a bachelor’s degree.

It feels like everyone I know doing some form of gig work complains from time-to-time of making crap wages. I tend to think the "desperation" you're seeing in people is more tied to structural economic issues vs. just plain stupidity. It's not that easy for some to just "find another good paying job," yet, in the meantime, they have bills to pay and/or savings they want to build.

For sure, I think some MSCs offer offensive/predatory compensation too. I don't think they can look at shoppers with a straight face and think $1.00 shops are totally fair. They are also just operating on supply and demand in the absence of a min. wage for the industry. And shoppers are desperate in America.

As someone who was very much alive 50 and 60 years ago I just want to mention that many low wage workers today have more than my solidly middle income family did back in those days. When I was growing up no one had closets and closets full of clothing and shoes..In fact if you ever walked into a house that was older you will notice the closets were very small...and they were not full. People wore their clothing until it was no good anymore. Middle class people took modest vacations, maybe a drive somewhere and a stay in a small cabin once a year. In fact vacation days were few per year. If someone had a car, it was not turned in every 3 years for a new one. Middle class people only ate out on occasion, maybe for a birthday and did not go to fast food restaurants constantly like now and.did not stock their freezers with gourmet specialties Kids played with neighborhood kids and did not own many toys or pay for lessons in things. We played with whatever we had on hand which was mostly our fantasies and games we made up with a simple rope or bat or one doll. Society and the media has turned wants into needs. Yes, those earning lower wages do not have what I have now. But back then if you were a low wage earner you lived with family or rented one room in a house with a shared bath down the hall. Middle class people lived modestly.

I do not think you can really compare what people have now vs then. People got by with a lot less then. To me the biggest issue is the cost of housing which is out of control in many areas.

I do not think you can really compare what people have now vs then. People got by with a lot less then. To me the biggest issue is the cost of housing which is out of control in many areas.

Keep in mind that wage and gig work are abundant in some places and scarce in others. Here, there are three grocery stores. How many local shoppers can complete local grocery shops every month, considering rotations? People who travel from towns an hour or so away might want to pick up shops while they are getting groceries, which are not available where they live. There are about twenty convenience/gas locations. How many shoppers can complete a convenience/gas shop every month? Well, if someone completes all of a convenience store for one month, the pay is [according to rumor] good. Even if you wait for a bonus and get it for a fast food, you are not earning a living here. At most, you are doubling or trebling your small outlay, using a few skills, and staying out of trouble for a few minutes. There are two McD's, three Subways, and one each of a smattering of other fast food joints and one-of-a-kind restaurants here. A few sports and auto dealerships survived, but we can't shop them often. Bonuses on a few shops do not add up to a living wage! To me, it makes sense to remove expectations for how people must mystery shop and declarations of what is the only acceptable pay for the work. Someone besides me needs to make it understood, okay, and even wonderful that people are working, as they can, in a place like this! No one should get away with judging what we must do to survive in a small town or to augment a more typical form of work. Rather, they should come, stay a season, and then determine what they have been able to do despite limited opportunities and constant awareness that some people actually need the little shop money that is here. Few local businesses can afford to pay what some shoppers will begin to consider. After one month, these visitors will be out of rotation for at least a month for most assignments. At the end of their visit, will they call us idiots? Or, will they slink away with their tails between their legs?

Pronoun, schmonoun. I am a female human.

I agree with you 10000% in comparing back then to now. I am 68 years old, and well remember how we grew up. You are spot on when you say media has turned wants into needs. We played with few toys but were never lacking to play with something. I can't tell you the number of hours we all in the neighborhood played "stick ball" with broom handles, "pinky" balls and 6 empty soup/veg cans - 3 lined up per side behind the batter, with a chalk circle drawn in front of the batter for the boundary to keep the stick in. We played for hours all summer long. So different now!@sandyf wrote:

As someone who was very much alive 50 and 60 years ago I just want to mention that many low wage workers today have more than my solidly middle income family did back in those days........

There used to be a grocery shop in my area with a $35 reimbursement but no fee. We need groceries, anyway. If they make me buy something I normally wouldn't then it has little value to me. If it's $35 I would have spent, anyway? I'll do it for that.

$9, $12, and $15- 7 , is not much. Think of it this way, you have to go on the board and find the shop.5 minutes, print materials for some shops,(I don't print MF's except once when they first change the questions) and I don't have to print TS's anymore since COVID. Then let's say it takes 10 minutes to drive there and 10 minutes to drive home, you are at 25 minutes in, then the assignment takes 20 minutes to go around all the different departments, you are at 45 minutes plus $3 dollars worth of gas and you are loaning them your 9-15 dollars for over a month. Then there is the matter of the 10-15 minutes it takes to input the report. So one hour of your time plus loaning them $9-15, and 3 dollars for gas. I think that is more than enough to deserve a measly $5 shop fee. Would you loan a million-dollar company money without interest too? They supposedly want the information to increase sales and make more money. But at whose expense? It's like those companies that don't care about their employees but steadily making millions.

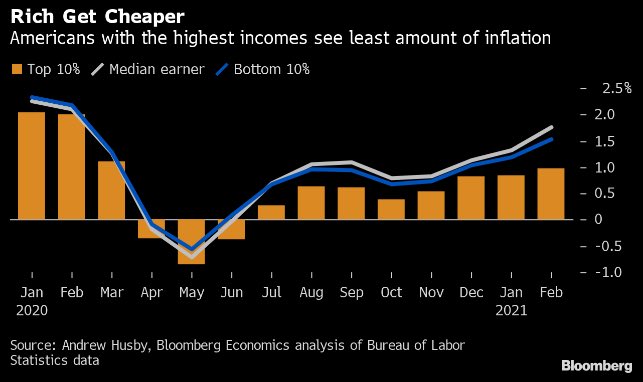

The rich even experience less inflation in many ways:

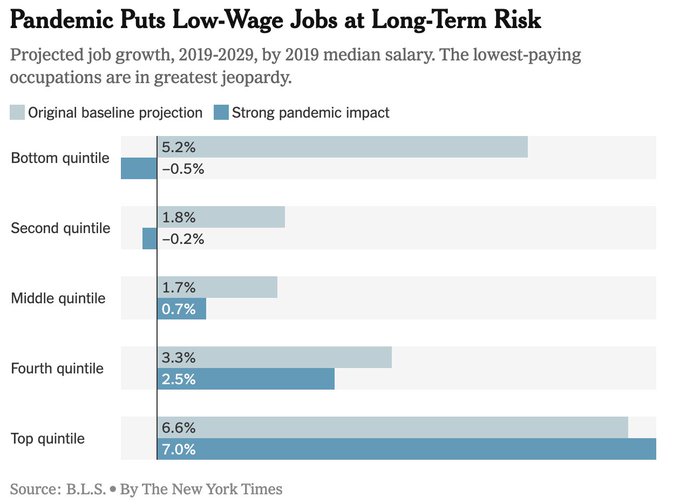

And this is as low-wage jobs prospects are looking more dim:

Edited 2 time(s). Last edit at 04/21/2021 03:00AM by shoptastic.

And this is as low-wage jobs prospects are looking more dim:

Edited 2 time(s). Last edit at 04/21/2021 03:00AM by shoptastic.

Well yes, this has been true Shoptastic. The rich only use a very small percentage of their wealth to purchase items that have inflated in price. The rest is in investments, most of which have done very well this past year. The low inocme on the other hand spend all their "wealth" so it is all hit by inflation. Although there has been very little price inflation during the few years it is coming now as businesses struggle to survive and recoup losses durings the pandemic. I just read that Proctor and Gamble expects to raise all prices in September. They are heavily into household staples.

A Robert Reich/NYT reference...yeah, not impartial data at all...puuu-lease!

The data IS impartial (those figures can be found anywhere) - even if you dislike Reich for whatever reasons.@maverick1 wrote:

A Robert Reich/NYT reference...yeah, not impartial data at all...puuu-lease!

Edited 1 time(s). Last edit at 04/21/2021 10:50PM by shoptastic.

That's part of it, although housing inflation has hit the rich too. It's just that:@sandyf wrote:

Well yes, this has been true Shoptastic. The rich only use a very small percentage of their wealth to purchase items that have inflated in price. The rest is in investments, most of which have done very well this past year. The low inocme on the other hand spend all their "wealth" so it is all hit by inflation. Although there has been very little price inflation during the few years it is coming now as businesses struggle to survive and recoup losses durings the pandemic. I just read that Proctor and Gamble expects to raise all prices in September. They are heavily into household staples.

a.) They often already have a house.

b.) So, b.), it's hitting them on their second...third...fourth houses.

The Bloomberg article that chart was pulled from had some interesting economist theories. One was that there are more competitors producing the things rich people like to buy. This lowers prices. Whereas, you see less competitors producing the things lower-income folks buy. ...I dunno if I buy this theory (partial pun intended), but it could be true.

Some other things are that the rich can stock up on things when they are on sale. My parents are notorious stock-pilers.

I'm talking a year's worth of TP, napkins, soap, etc. if they see it on sale. A person living paycheck-to-paycheck may have to buy x/y/z at whatever price (they may not have time/money to travel to get the best deals either) when they immediately need it.

I'm talking a year's worth of TP, napkins, soap, etc. if they see it on sale. A person living paycheck-to-paycheck may have to buy x/y/z at whatever price (they may not have time/money to travel to get the best deals either) when they immediately need it.

Credit lending standards are tighter (sometimes for good reason, though) for them as well.

My score is the highest it's ever been and it has taken me like three months of paying everything down to finally start getting credit line increases. and about 3k paid off.

Lending standards also tend to tighten during recessions - not just b/c one has a lower income, a low credit score, etc. - it's just one of those typical macro-economic environmental factors. Banks are more skeptical of people's ability to pay when the overall economy is doing very poorly. Not your fault, necessarily.@F and L TeleComm wrote:

My score is the highest it's ever been and it has taken me like three months of paying everything down to finally start getting credit line increases. and about 3k paid off.

Oh, but wait...if you're a hedge fund on Wall Street, it's been great for you! *eye-roll*

You can get money any time you want. And if something catastrophic happens with your Wall Street gambling that crashes the economy? No worries. Main Street taxpayers will bail out Wall Street as always, since they are major donors to Congress.

Remember that Trix slogan: "Silly rabbit, Trix are for kids."

There should be a credit/bailout one: "Silly peasant, credit and bailouts are for the rich."

Edited 2 time(s). Last edit at 04/22/2021 12:14AM by shoptastic.

[www.reuters.com]@ wrote:

"There’s been no shortage of credit provided overall by U.S. banks in the last year. It’s just that most of it went to Wall Street rather than Main Street."

So today I had two local shops and eleven more of the same in a city an hour away.

If I had more time and energy, I could have added about $150 to the day. I and my back pooped out about two hours before I finished the basic planned work. But if I could do this every day, I would be well on the way to IC prosperity!

I merely mention it to highlight the differences between places and backs.

If I had more time and energy, I could have added about $150 to the day. I and my back pooped out about two hours before I finished the basic planned work. But if I could do this every day, I would be well on the way to IC prosperity!

I merely mention it to highlight the differences between places and backs.

Pronoun, schmonoun. I am a female human.

@shoptastic...it's American business. I grew up with two other siblings by a divorced mother who was a secretary for a business. We didn't have much. But I had a fun childhood. Alimony was $10 per week per child. Vacations were spent camping. I still have my first 10-speed bike. I'm the 1st to graduate from college (and without debt too). Mom only had a mortgage and a car loan. No credit card debt. After starting work for American businesses, I've always saved at least 25% of my paycheck to 401K or after-tax investments in other American businesses (e.g. S&P500). My investments in American businesses for decades enabled me to accumulate several million dollars and to retire 14 years before my normal SS retirement date. From nothing. Go Wall Street! Go Main Street! Go America! [...but I will agree that the lobbyist industry inside the beltway should be dismantled]

Are higher fees and tax impacts the only way to respect shoppers? What about shops that pay no fees but reimburse shopper-selected groceries? I could become accustomed to a reimbursement of, say, fifty to sixty dollars of groceries per shop. All of the flavor and none of the tax. Hmm.

Pronoun, schmonoun. I am a female human.

@F and L TeleComm wrote:

$9, $12, and $15- 7 , is not much. Think of it this way, you have to go on the board and find the shop.5 minutes, print materials for some shops,(I don't print MF's except once when they first change the questions) and I don't have to print TS's anymore since COVID. Then let's say it takes 10 minutes to drive there and 10 minutes to drive home, you are at 25 minutes in, then the assignment takes 20 minutes to go around all the different departments, you are at 45 minutes plus $3 dollars worth of gas and you are loaning them your 9-15 dollars for over a month. Then there is the matter of the 10-15 minutes it takes to input the report. So one hour of your time plus loaning them $9-15, and 3 dollars for gas. I think that is more than enough to deserve a measly $5 shop fee. Would you loan a million-dollar company money without interest too? They supposedly want the information to increase sales and make more money. But at whose expense? It's like those companies that don't care about their employees but steadily making millions.

Finally! Someone who gets it!

So people who have little resources are expected to demand more in fees which might raise their tax bill later. How is that good?

Pronoun, schmonoun. I am a female human.

So people who have little resources are expected to demand more in fees which might raise their tax bill later. How is that good?

Not all people have an equal opportunity to turn things around with mystery shops and similar gigs. Kudos to those who can do that. Perhaps they have transportation for lucrative routes, access to plenteous gigs, or schedules that are favorable to gigs. These are good things, but not all people have them equally.

The people who cannot change their lives to a great extent via the few gigs they can access should not be castigated for their circumstances. Rather, it should be understood that all workers have unique situations for which demands, expectations, and formulae do not apply equally if at all. And the demands, expectations, and formulae should be obliterated.

Not all people have an equal opportunity to turn things around with mystery shops and similar gigs. Kudos to those who can do that. Perhaps they have transportation for lucrative routes, access to plenteous gigs, or schedules that are favorable to gigs. These are good things, but not all people have them equally.

The people who cannot change their lives to a great extent via the few gigs they can access should not be castigated for their circumstances. Rather, it should be understood that all workers have unique situations for which demands, expectations, and formulae do not apply equally if at all. And the demands, expectations, and formulae should be obliterated.

Pronoun, schmonoun. I am a female human.

Would someone with so few resources be concerned about a tax bill? Or would they be concerned about getting food on the table, gas in the car and other things MSing can offer?

@Shop-et-al wrote:

So people who have little resources are expected to demand more in fees which might raise their tax bill later. How is that good?

"I told myself to quit you; but I don't listen to drunks." -Chris Stapleton

They should be so concerned. The IRS charges interest for payment plans. People with scant resources might find it difficult to pay a tax bill they incurred from IC revenue and insufficient deductions. It would be even more difficult to stretch out the payments and pay interest on top of the bill. They would be trapped unless they consistently were top earners who simultaneously generated sufficient deductions.

There is a weird sort of poverty math. It is not so easy to get out and stay out of poverty. Significant MS-ing or other IC income will help some people to improve their lives substantially. It will hurt others. There is also readiness. Some people are ready to change their lives and move beyond benefits. Others are not.

Even if some IC's here believe that everyone should be paid more, none of us knows what the impact of higher feels will be for each IC.

There is a weird sort of poverty math. It is not so easy to get out and stay out of poverty. Significant MS-ing or other IC income will help some people to improve their lives substantially. It will hurt others. There is also readiness. Some people are ready to change their lives and move beyond benefits. Others are not.

Even if some IC's here believe that everyone should be paid more, none of us knows what the impact of higher feels will be for each IC.

Pronoun, schmonoun. I am a female human.

I don't understand. Taxes are paid on profits. More profits are usually good, even if a small portion has to go to taxes.

There it is. For some people, even the "small portion" is a burden. There really are people who will not be able to earn so much money consistently that taxes become as nothing and poverty evaporates along with the need for any assistance or benefits. To me, it seems wicked to castigate or blame strangers about whom we know nothing, especially when those people might be making the best of their situations-- even if better or best does not resemble how we work or live.

Pronoun, schmonoun. I am a female human.

Taxes are the price we pay to live here. American freedom is not free.

Each of us has a path we can follow. Some start at different points on the path. My wife and I started by moving in together into a single mobile home. Worked and saved. Went to school at night. Worked and saved. Bought a house. Worked and saved. Finished our degrees. Got raises. Kept working and saving. Fixed cars and houses and took care of our yard ourselves. Never had cable. Only the lowest cost phone plans. Now we gain more from our investments than from working so we retired early. Our investments gained about $6K in the stock market on 6/4. Other days it might go down, but more likely up. I don't worry about mystery shopping fees, but I prefer them. Certainly don't need them. It's just another frugal hack. Part of being a Maverick.

Edited 1 time(s). Last edit at 06/05/2021 09:03PM by maverick1.

Edited 1 time(s). Last edit at 06/05/2021 09:03PM by maverick1.

Sorry, only registered users may post in this forum.